Howie/iStock via Getty Images

By Eva Mante

China’s economic recovery has stalled

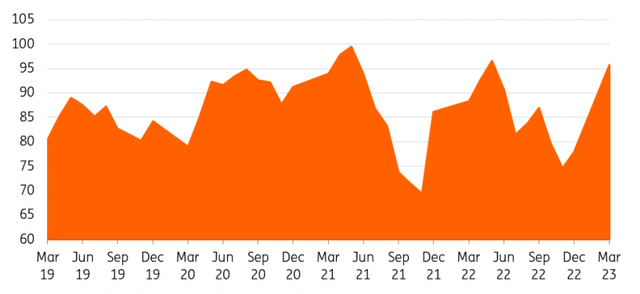

Iron ore has been in decline for almost two months. Its price on the Singapore Exchange fell to a record low of $94.20/t last week, down more than 20% year-to-date. Highs and now hovering below the key $100/t level.

Prices rose above $130/t in February amid challenges to a revival of steel demand in top consumer China following the end of severe Covid-19 lockdowns.

Although China reported annual quarterly GDP growth of 4.5% last month, ahead of expectations – and much faster than the 2.9% for Q422 – there are concerns about whether the pace of growth will be sustained. China’s manufacturing activity slowed in April, with the Purchasing Managers’ Index falling to 49.2 in April from 51.9 in March, a warning signal for the Chinese economy. This followed three consecutive months of growth 2023 start.

Growth in the construction sector, which accounts for half of China’s steel demand, has also been slower than expected. New property starts fell 29.1% in March compared to the same period a year earlier.

Meanwhile, consumer inflation in China fell to near zero in April, its weakest pace in two years, while producer prices fell further on deflation, adding to concerns about a weak demand recovery in the country.

Iron ore slips below $100/t

SGX, ING Research

China’s steel consumption is disappointing

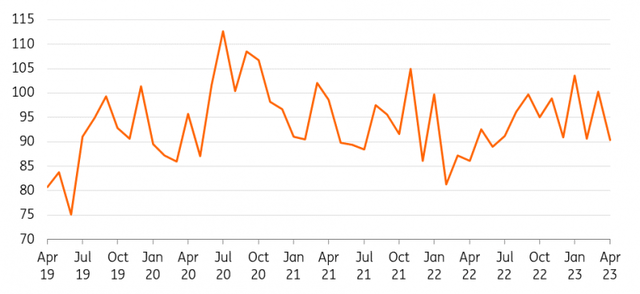

Steel consumption in China typically disappoints during the country’s peak construction season. March and April are usually the peak production months of the Chinese steel market. The latest data from the China Iron and Steel Association (CISA) showed steel inventories at major Chinese steel mills fell to 18.1mt in late April, down 2.3% compared to mid-April.

Similarly, crude steel production at major plants fell by 3.6% in the period to 2.21mt/d at the end of April.

Amid disappointing demand, steel mills have been forced to cut prices to dying levels. China Bao Steel, China’s leading steelmaker, has cut its factory-gate prices with at least two mills, according to MySteel. Meanwhile, steel mills in Fengnan District of Dongshan City have been officially asked by local authorities to limit crude steel production. This is the first batch of steel mills in China after repeatedly cutting crude steel output in 2021 and 2022.

Chinese authorities are reportedly considering an official target of cutting steel production by 2.5% by 2023.

According to data from the World Steel Association, China’s steel production fell 2% to 1.0 billion tonnes last year, mainly due to government-ordered production cuts.

China looks set to continue to curb crude steel production while replacing aging steel capacity with electric arc furnace capacity to help the country meet its decarbonization goals. Electric arc furnace (EAF) capacity growth at the expense of basic oxygen furnace (BOF) capacity will be a concern for the medium to long-term outlook for Chinese iron ore demand. It also suggests that we have already seen China’s iron ore imports peak in 2020.

China’s Monthly Crude Steel Production (Million Tons)

WSA, ING Research

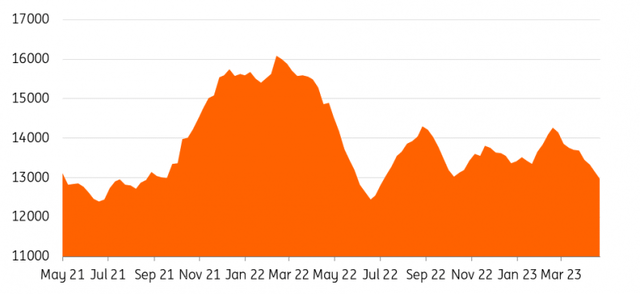

China’s iron ore imports are sluggish

Iron ore imports are also under pressure this year as steel consumption from China has declined. China’s iron ore purchases fell to a 10-month low in April, a sign of slowing demand.

China imported 90.44 million tonnes of iron ore in April, more than 100 million tonnes in March and the lowest since June 2022, customs data showed. Iron ore reserves have also fallen. Total iron ore stocks at ports in China fell 11% year-on-year to 129.2 million tonnes. China’s iron ore port inventory is a key indicator that reflects the supply and demand balance, as well as the safety net and imbalance between iron ore supply and steel plant demand.

As the peak construction season draws to a close, there is little upside for steel production and iron ore demand recovery in the short to medium term, with expected demand recovery not meeting expectations.

China’s monthly iron ore imports (million tonnes)

NBS, ING Research

China Iron Ore Total Ports Stock (10000 Metric Tons)

Steelholm, ING Research

Supply increases from majors

The supply side has remained firm so far this year. Rio Tinto ( RIO ), the world’s largest iron ore producer, reported a better-than-expected 15.4% improvement in Q1 iron ore exports from Western Australia, a record for the quarter, as production increased at its Gudai-Darri mine. Its Pilbara operations produced 79.3 million tonnes of iron ore in Q1 2023, up 11% from Q1 2022.

Also, Vale SA ( VALE ) reported a 5.8% year-on-year increase in Q1 iron ore production due to strong performance at S11D. The company produced 66.77 million tonnes of iron ore in the first three months of 2023.

Meanwhile, BHP ( BHP ) maintained its iron ore production guidance of 249 million to 260 million tonnes for the full year, reaching 191.7 million tonnes of iron ore year-to-date, with the March quarter contributing 59.8 million tonnes.

Government inspection may control prices

Iron ore’s sharp price moves have drawn scrutiny and warnings from regulators. The National Development and Reform Commission (NDRC) last month said it would closely monitor the dynamics of the iron ore market and take steps to curb price hikes. Since the beginning of the year, the NDRC and other authorities have improved joint supervision and regulation of the iron ore market to curb price gouging, excessive speculation and illegal activities.

Earlier, government interventions to calm markets included suppressing trade and ordering steel capacity cuts. If we see similar measures being used again, this could add further negative pressure to our outlook.

We believe the short-term outlook for iron ore is less bearish, with sluggish demand from China suggesting prices should stay low. We expect prices to average $100/t in Q4 and $106/t in 2023, and prices will remain volatile as the market continues to respond to any policy changes by the Chinese government.

Content disclaimer

This publication is prepared by ING for informational purposes only, without regard to the means, financial situation or investment objectives of a particular user. This information does not constitute an investment recommendation and is not investment, legal or tax advice or an offer or solicitation to buy or sell any financial instrument. Read more

Editor’s note: Summary bullets for this article were selected by Seeking Alpha editors.

Looking for an expression of alpha: Past performance is no guarantee of future results. No recommendation or advice is given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above do not necessarily reflect the opinion of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third-party writers, including both professional investors and individual investors who are not licensed or certified by any agency or regulatory body.

„Oddany rozwiązywacz problemów. Przyjazny hipsterom praktykant bekonu. Miłośnik kawy. Nieuleczalny introwertyk. Student.